The Death of Cash by a Thousand Cuts

Across Britain, the infrastructure of physical money is being quietly dismantled. Since 2015, over 5,000 bank branches have closed, leaving entire communities without access to basic financial services. ATMs are vanishing at a rate of 300 per month. Meanwhile, an increasing number of businesses — from coffee shops to car parks — display the now-familiar 'card only' signs, treating cash like a relic from a bygone era.

This isn't happening by accident. It's the result of deliberate choices by financial institutions and policymakers who frame the elimination of cash as inevitable technological progress. But progress for whom?

Who Gets Left Behind

The rhetoric of a 'cashless society' conveniently ignores the 2.4 million adults who remain unbanked or rely primarily on cash for their daily transactions. These aren't Luddites clinging to outdated habits — they're people for whom digital payments represent genuine barriers.

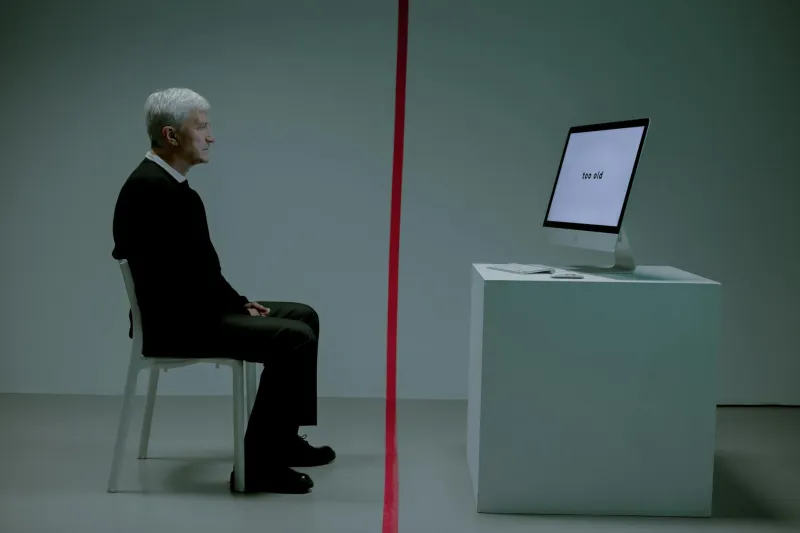

The elderly, who make up 60% of cash users, often lack the digital literacy or smartphone access that cashless systems demand. People with disabilities may find chip-and-pin terminals physically inaccessible or struggle with banking apps that weren't designed with their needs in mind. Those experiencing domestic abuse use cash to maintain financial independence from controlling partners who monitor card transactions.

Perhaps most significantly, cash remains the primary budgeting tool for people on low incomes. The Joseph Rowntree Foundation found that families in poverty are three times more likely to rely on cash because it provides immediate, tangible control over limited resources. When you're counting every pound, the psychological difference between handing over physical money and tapping a card can mean the difference between staying within budget and falling into debt.

The Profit Motive Behind 'Progress'

The push toward cashless payments isn't driven by consumer demand — it's driven by corporate profit margins. For banks, cash is expensive. ATMs require maintenance, branches need staff, and physical currency must be transported and secured. Digital transactions, by contrast, generate fees while shifting operational costs onto consumers and small businesses.

Payment processing companies like Visa and Mastercard have spent millions lobbying against cash acceptance requirements, framing their opposition as support for 'innovation.' Their business model depends on extracting a percentage from every transaction — something impossible with cash payments.

Meanwhile, fintech companies have rebranded financial exclusion as 'financial inclusion,' promoting digital-only solutions that require smartphones, stable internet connections, and comfort with technology that many vulnerable people simply don't have.

The Hidden Costs of Going Cashless

When businesses refuse cash, they're not just inconveniencing customers — they're imposing a regressive tax on the poorest. Small businesses forced to adopt card-only policies pass processing fees onto consumers through higher prices. The Federation of Small Businesses estimates these fees cost retailers £1.3 billion annually.

For consumers, the costs are less visible but equally real. Bank account fees, overdraft charges, and the need for smartphones and data plans create barriers that cash doesn't impose. A simple transaction that once cost nothing now requires navigating a web of corporate intermediaries, each taking their cut.

The surveillance implications are equally troubling. Every digital payment creates a permanent record, building detailed profiles of individual spending patterns that can be accessed by corporations, governments, and data brokers. Cash, by contrast, preserves privacy and autonomy — qualities that seem increasingly quaint in an age of ubiquitous monitoring.

International Lessons We're Choosing to Ignore

Other European countries have recognised these risks and acted accordingly. Sweden, despite being a global leader in digital payments, has legislated to ensure cash acceptance after recognising the exclusion it was creating. The European Central Bank has explicitly warned against the elimination of cash, citing concerns about financial inclusion and monetary sovereignty.

Photo: European Central Bank, via photos.wikimapia.org

Photo: European Central Bank, via photos.wikimapia.org

Germany, meanwhile, has maintained strong cash usage alongside digital innovation, understanding that true choice means preserving alternatives rather than forcing convergence on a single payment method.

A Public Health Emergency in Disguise

The COVID-19 pandemic accelerated cashless adoption under the banner of public health, but the emergency measures have become permanent policies. Research by the University of Oxford found no evidence that cash presents meaningful transmission risks when basic hygiene is observed, yet 'hygiene' became a convenient justification for policies that primarily benefit corporate interests.

The real public health crisis is financial exclusion itself. When people can't access basic services because they lack digital payment methods, the consequences cascade through housing, healthcare, and social participation. The stress of navigating an increasingly hostile financial environment contributes to mental health problems that our already-strained NHS must then address.

The Choice We're Not Being Given

The framing of cashless society as inevitable obscures the reality that this is a political choice. We could require businesses to accept legal tender. We could mandate that essential services remain accessible to cash users. We could treat payment diversity as a matter of equality rather than efficiency.

Instead, we're allowing market forces to eliminate options for the most vulnerable while calling it progress. The irony is stark: in an age of supposed financial innovation, we're moving toward a less inclusive, more expensive, and more surveilled system than the one we're replacing.

The cashless society isn't coming — it's being built, brick by brick, by interests that profit from excluding the poor and calling it modernisation.